What is ESG?

ESG, shorthand for “Environmental, Social, Governance” encapsulates the growing expectation for corporations to uphold ethical standards in these domains. Various frameworks have been established to evaluate and disclose their ESG performance.

ESG mirrors the “triple bottom line” conceptualization of sustainability [1]. This approach maintains that sustained viability, whether of a business or a civilization, rests on three pillars: people, planet, and profit.

Why is ESG important?

ESG reporting serves corporations and their stakeholders, including financial institutions, as a tool for identifying and evaluating business risks and opportunities within the ESG domains. ESG reports provide investors with insights into whether a company’s values align with its priorities. Consequently, ESG performance became an important criteria in investment decisions.

Moreover, sustainability initiatives can yield multiple benefits. They can drive down operational costs, mitigate risks associated with ESG issues like climate change, and unlock new marketing avenues.

Now, let’s briefly delve into the most important environmental, social, and governance challenges companies face, before we introduce the ESG reporting frameworks.

Environmental criteria

While there are many environmental concerns, some tend to get the most attention in ESG reporting:

- Climate change

- Water use

- Biodiversity

- Deforestation

- Raw material- and fossil-fuel depletion

- Waste & toxic emissions

- Plastic pollution

Corporations should not solely report the impacts of their operations or products but also assess their vulnerability to environmental risks. They should consider, for example, if climate change poses business risks (such as the threat of sea level rise affecting coastal production sites), or if the possible future scarcity of water and fossil fuels could substantially raise production costs.

Social criteria

Social criteria address a company’s relationship with people and institutions in the communities where it operates.

Considerations include:

- Fair wages

- Compliance with labor laws (also regarding modern slavery)

- Impact and contributions to affected communities

- Workers health, safety, and opportunities to develop

- Diversity, Equity, and Inclusion

- Customer privacy and data security

Governance criteria

The governance component of ESG evaluates how a company is run, and how able the leadership is to steer the organization in a sustainable direction. Robust governance practices are critical for building stakeholder trust, managing identified ESG risks, and long-term value creation.

Governance criteria include:

- Board Composition & Diversity

- Executive compensation, e.g. using CEO-to-median employee pay ratios

- Regulatory compliance

- Risk management practices

- Financial transparency, taxation, and anti-corruption practices

- Stakeholder participation opportunities

ESG regulations and frameworks

As you’ve probably noticed, ESG criteria cover a lot of ground. But do companies have to report on everything? And how can they understand and measure their performance? That’s where regulations and reporting frameworks come into play!

Through “materiality assessments” integrated within ESG frameworks, companies gain clarity on which ESG issues they need to address most urgently. “Materiality”, conceptualizes how relevant or significant an issue is to a business.

Corporate Sustainability Reporting Directive (CSRD)

Since January 5th, 2023, the EU has mandated ESG reporting through its CSRD (EU 2022/2464). This applies to large companies, all listed companies (excluding micro-enterprises), and some non-EU companies. They must conduct a double materiality assessment* to identify the most relevant ESG issues for reporting [2]. Reporting must adhere to the European Sustainability Reporting Standards, the latest version of which is available here [3].

*A ‘double materiality assessment’ evaluates both how a company affects people and the planet (termed ‘impact materiality’), and how ESG issues generate financial risks and opportunities for the company (‘financial materiality’).

Are there other ESG regulations?

The CSRD is part of the EU Green Deal and is the most comprehensive regulation enforcing ESG reporting across the EU. It builds upon the earlier, less comprehensive EU ESG reporting scheme known as the Non-Financial Reporting Directive, which came into force in 2018. Additionally, there are specific ESG reporting requirements in place for the financial sectors of the EU and UK, as well as for enterprises in Germany and the UK. You can find a helpful overview here.

Carbon Disclosure Project (CDP)

The Carbon Disclosure Project (CDP) focuses on environmental issues like climate change, water usage, deforestation, plastic pollution, and biodiversity. It started in the UK back in 2000 with a focus on greenhouse gas emissions but has since grown to have offices in 50 countries, expanding its scope to various environmental concerns. Over half of the global capital market’s value comes from companies that report through CDP [4].

Reporting requirements vary based on factors such as sector, company size, and activities. Companies report their emissions to CDP through a questionnaire, and CDP evaluates their performance using a grading scheme similar to school grades (A-F, where A is the best) [5]. CDP then publishes these scores and reported emissions on its website and compiles reports based on them.

CDP publications inform some financial institutions to make sustainable investments. Some reports are compiled on behalf of these institutions, and CDP may also request companies to report their emissions for specific reports. However, reporting to CDP is always voluntary.

To measure and report carbon emissions embedded in products, Life Cycle Assessment (LCA) and verified Environmental Product Declarations (EPDs, resulting from LCA) are recommended [6].

Global Reporting Initiative (GRI)

The GRI is the go-to framework for voluntary reporting on ESG issues. It’s widely used by over 70% of companies worldwide.

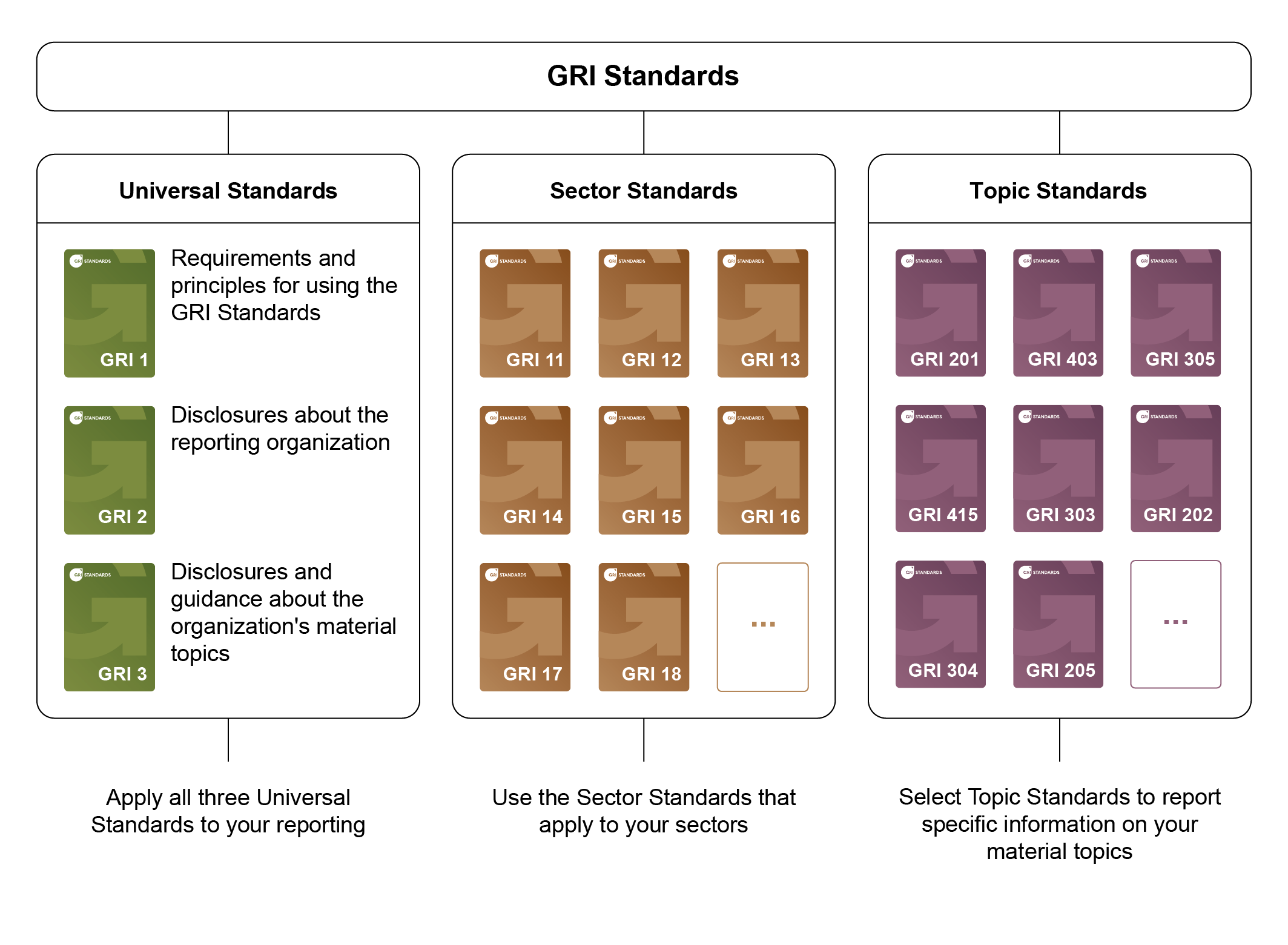

GRI offers different but interconnected reporting standards (full list):

- General (Standards 1-3): These are the basis for ESG reporting, requiring disclosures on a company’s structure and material issues. They guide companies which other GRI standards to consider.

- Sector (Standards 11-14): These are specific to major sectors like oil and gas, coal, agriculture, and mining. More sectors will be added later.

- Topic (Standards 101-418): These focus on individual topics within ESG. For environmental concerns, standards 101-308 are applicable. If a company needs to report on the environmental impact of its products, it might use LCA. LCA is the internationally agreed upon scientific method to measure the environmental impacts of products.

The GRI standards have been developed in consultation with stakeholders and experts in respective sectors and topics, and thus reflect the markets’ expectations regarding reporting.

In the general standards, companies are encouraged to adhere to applicable sector standards and relevant topic standards. While they can choose to select specific topic standards and omit others that may be mandatory for their sector, doing so means they are not fully compliant with GRI. However, they can still benefit from GRI’s guidance on the chosen topics [7].

Overview of GRI standards [8]

How to get started with ESG reporting?

To start with ESG reporting, here’s a simple guide:

- Check if the CSDR applies to your company. If it does, you must follow the European Sustainability Reporting Standards – it’s mandatory!

- If the CSDR doesn’t apply to you, you have more flexibility. Among the voluntary standards, the most comprehensive one is the GRI framework.

- However, if you already know your significant issues and they are all covered in the CDP, this framework might be more relevant for your company.

If you want to deeply understand and report on the environmental impacts of your products, consider using Ecochain LCA software. It offers a user-friendly way to conduct LCA, providing insights into which aspects of your products cause the most environmental impacts. This information can guide you in taking effective actions to improve your environmental performance.

[cta cta_id=”3171″]

References

[1] Kenton, W. (2023, December 17). Triple Bottom Line. Investopedia. https://www.investopedia.com/terms/t/triple-bottom-line.asp#:~:text=The%20triple%20bottom%20line%20is%20an%20accounting%20framework%20that%20incorporates,planet%2C%20and%20profit.%222

[2] King & Spalding. (2024, January 31). The New EU Corporate Sustainability Reporting Directive: What Does It Mean For Non-EU Companies?. https://www.kslaw.com/news-and-insights/the-new-eu-corporate-sustainability-reporting-directive-what-does-it-mean-for-non-eu-companies

[3] European Commission. (n.d.). Corporate sustainability reporting. https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en

[4] CDP. (2022, October 19). Nearly 20,000 organizations disclose environmental data in record year as world prepares for mandatory disclosure. https://www.cdp.net/en/articles/media/nearly-20-000-organizations-disclose-environmental-data-in-record-year-as-world-prepares-for-mandatory-disclosure

[5] Net0. (2024, February 28). Carbon Disclosure Project (CDP) Reporting: Facts to Get You Started. https://net0.com/blog/cdp-reporting

[6] Carbon Leadership Forum. (n.d.). Guidance on Embodied Carbon Disclosure. https://carbonleadershipforum.org/guidance-on-embodied-carbon-disclosure/

[7] GRI. (n.d.). A Short Introduction to the GRI Standards. https://www.globalreporting.org/media/wtaf14tw/a-short-introduction-to-the-gri-standards.pdf

[8] GRI (n.d.) [Image].

{kind=link}